K I T E M O R T G A G E S

Specialist mortgage broker

for City professionals

We work with lawyers, investment bankers, private equity and hedge fund professionals, traders, and senior tech leaders.

We structure mortgages around complex income — bonuses, RSUs, carried interest, partnership drawings, and foreign currency. If your income doesn't fit a standard model, we know which lenders will treat it properly.

Y O U R T E A MEvery client speaks directly with an adviser who already knows how your income is assessed — and which lenders treat it most favourably

David Walsh

Director & Mortgage Broker

Founder of Kite Mortgages. Specialist in complex income structures for City professionals. Advises on mortgage strategy for high earners with partnership income, bonus-heavy pay, equity compensation, and foreign currency earnings.

View profile →

Simon Hart

Mortgage & Protection Adviser

Mortgage adviser at Kite Mortgages. Specialises in high-value purchases and remortgages for City professionals. Works with clients navigating complex income structures including variable pay, carried interest, and multi-currency earnings.

View profile →W H O W E H E L PFind your profession

We specialise in six areas where income complexity most often affects mortgage outcomes. Each has its own challenges — and we know how to navigate every one of them.

01

Lawyers & Law Firm Partners

Partnership drawings, profit share, and LLP structures assessed accurately — from NQ solicitors to Magic Circle equity partners.

Learn more →

02

Investment Banking Professionals

Bonus-heavy income treated fairly. We know which lenders will use your full bonus history — not just average it down.

Learn more →

03

Private Equity Professionals

Carried interest, co-invest, and deferred compensation require lenders who understand fund economics, not just payslips.

Learn more →

04

Hedge Fund Professionals

Performance-linked pay that varies dramatically year on year. We structure applications around your strongest provable position.

Learn more →

05

Trading & Investment Professionals

Risk-based pay, structurer income, and market-linked bonuses rarely fit standard affordability models. We know which do.

Learn more →

06

Tech & Product Leaders

RSUs, stock options, and international equity packages need specialist lender treatment — especially with USD or EUR income.

Learn more →

W H A T W E U N D E R S T A N D

We structure mortgages around complex income

Standard lenders use standard models. If your income doesn't fit the template, you borrow less than you should. We know exactly where the flexibility is — and which lenders offer it.

We don’t just place mortgages. We understand how your income works and which lenders will treat it fairly. That’s the difference between the right mortgage and a compromised one.

H O W I T W O R K S

From first call to completion

We keep the process simple. Most clients receive indicative figures within the first conversation.

C L I E N T R E V I E W S

What our clients say

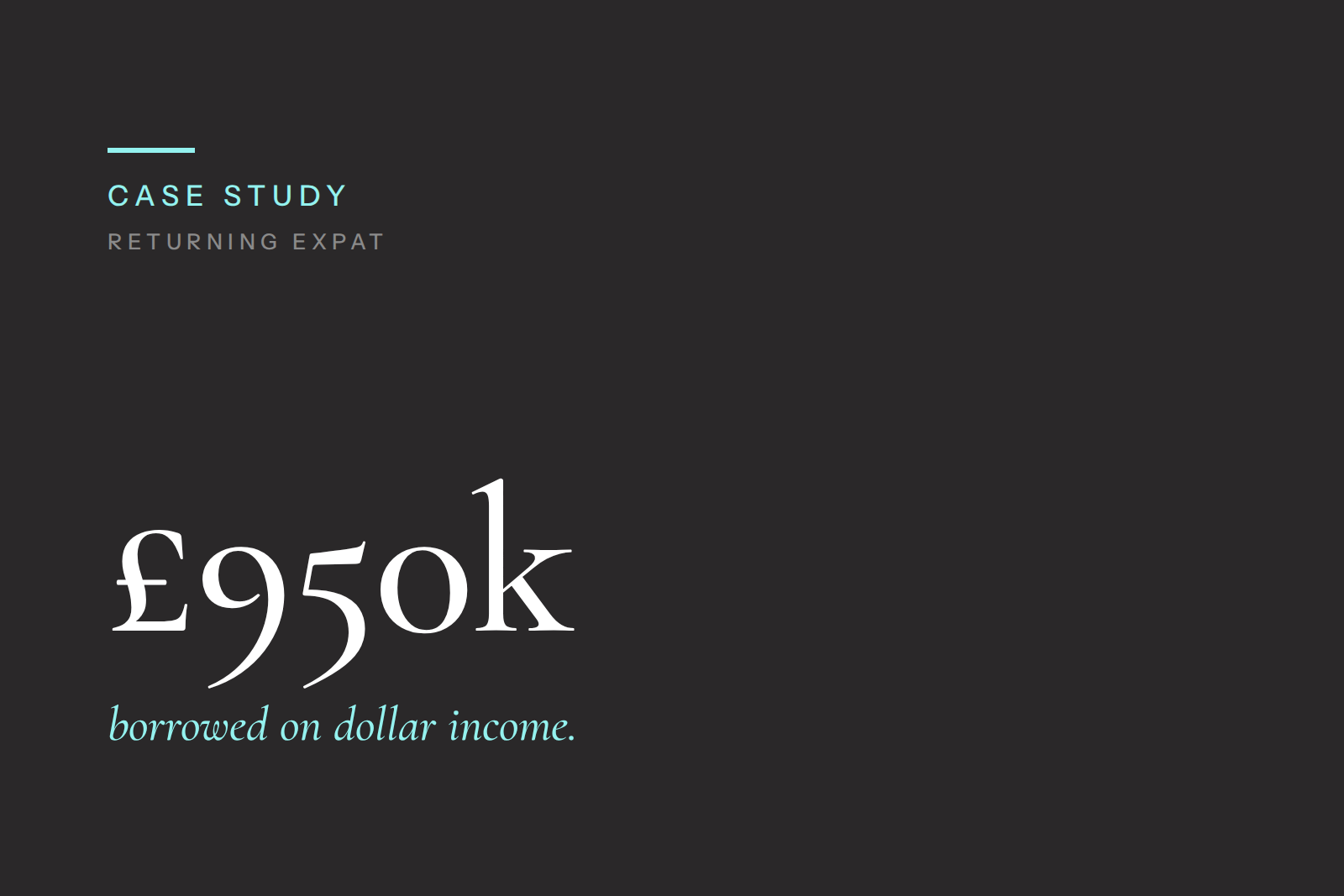

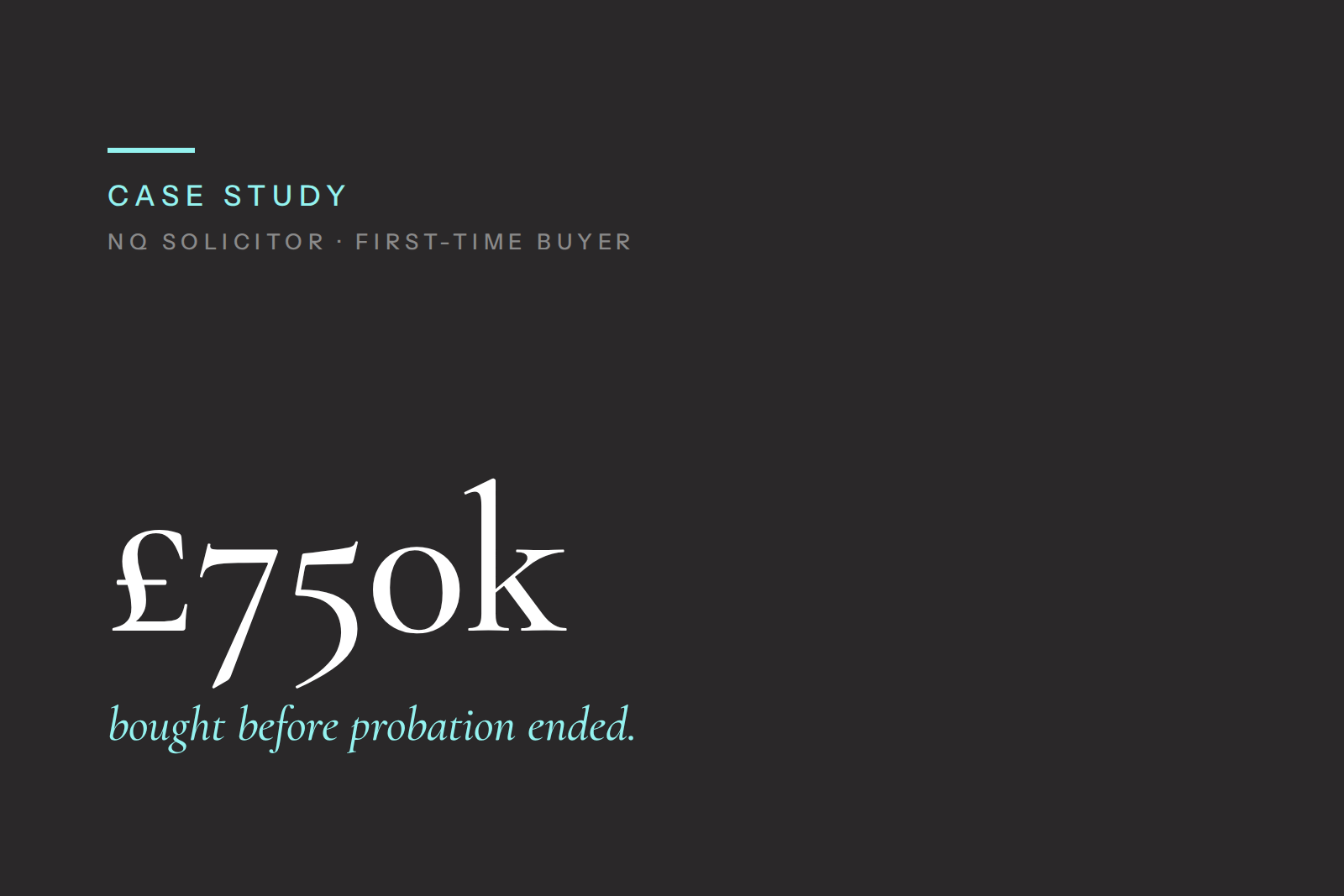

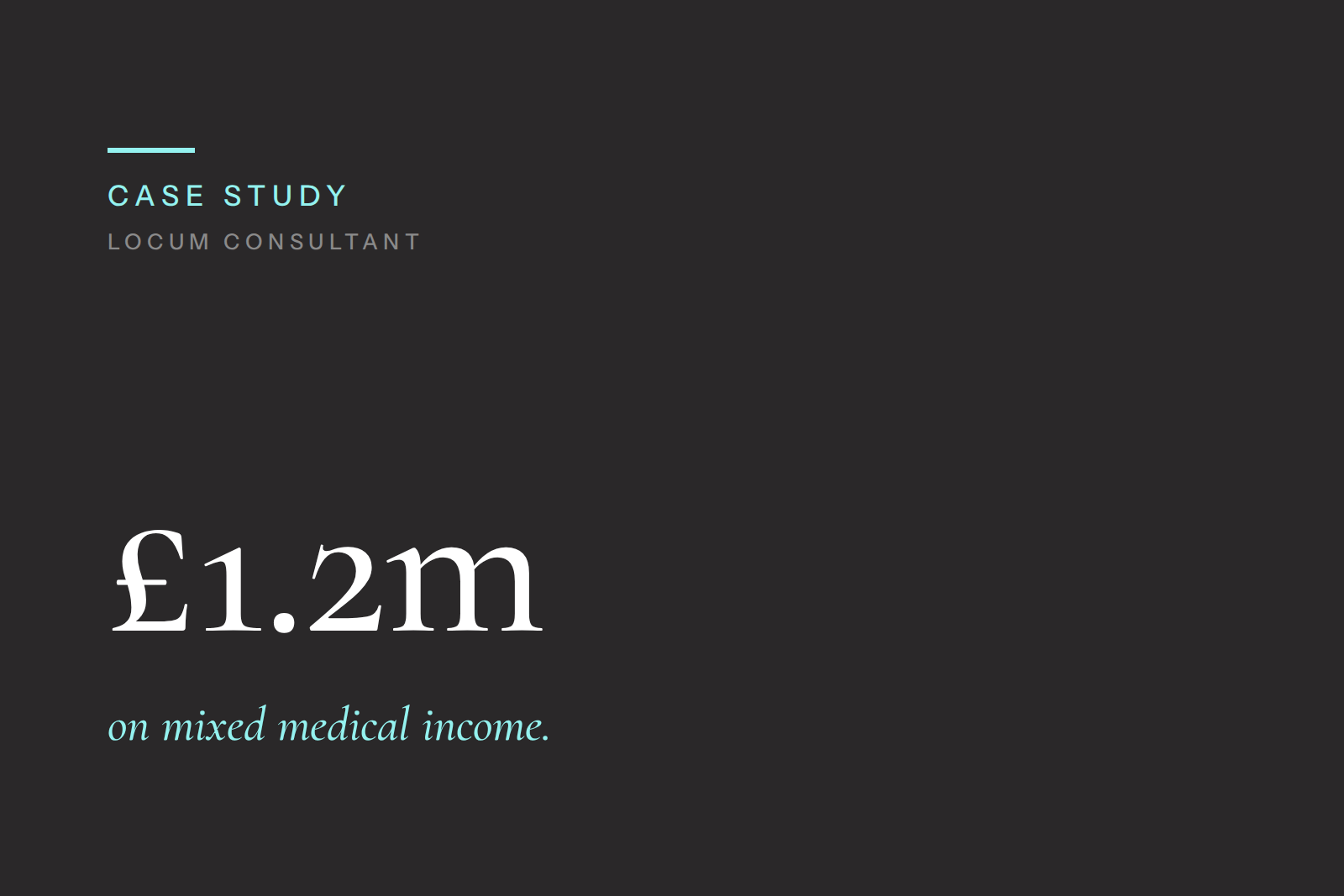

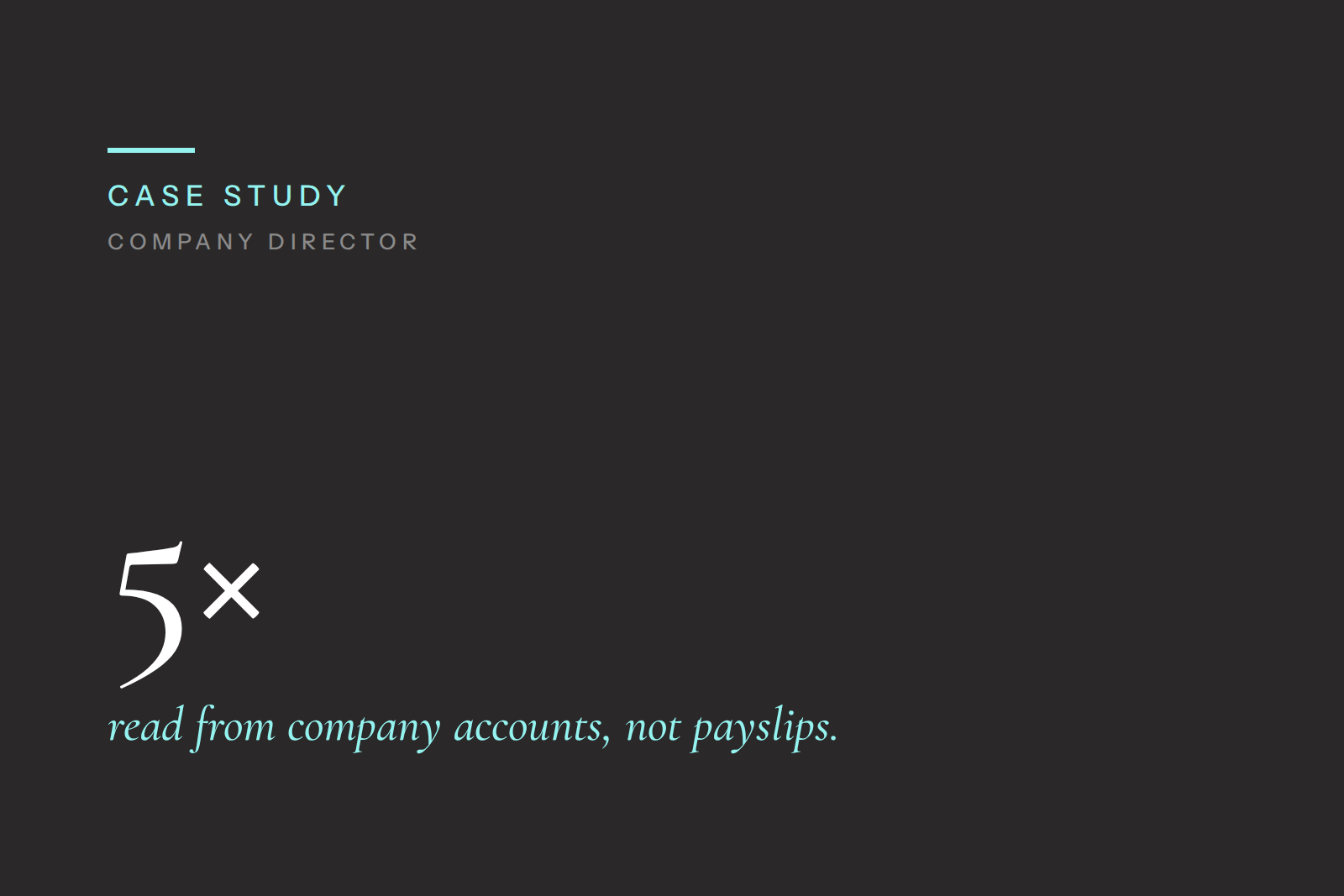

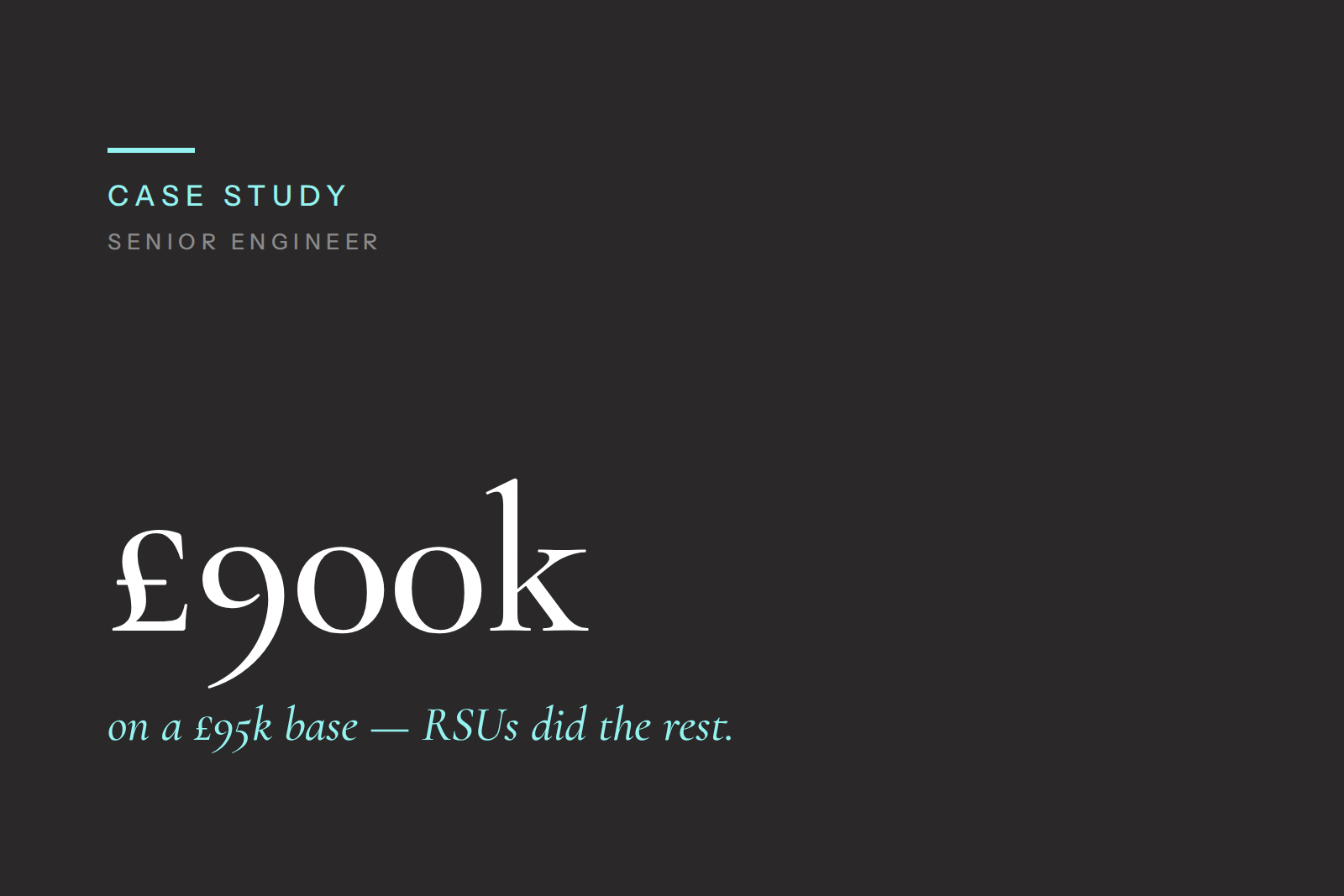

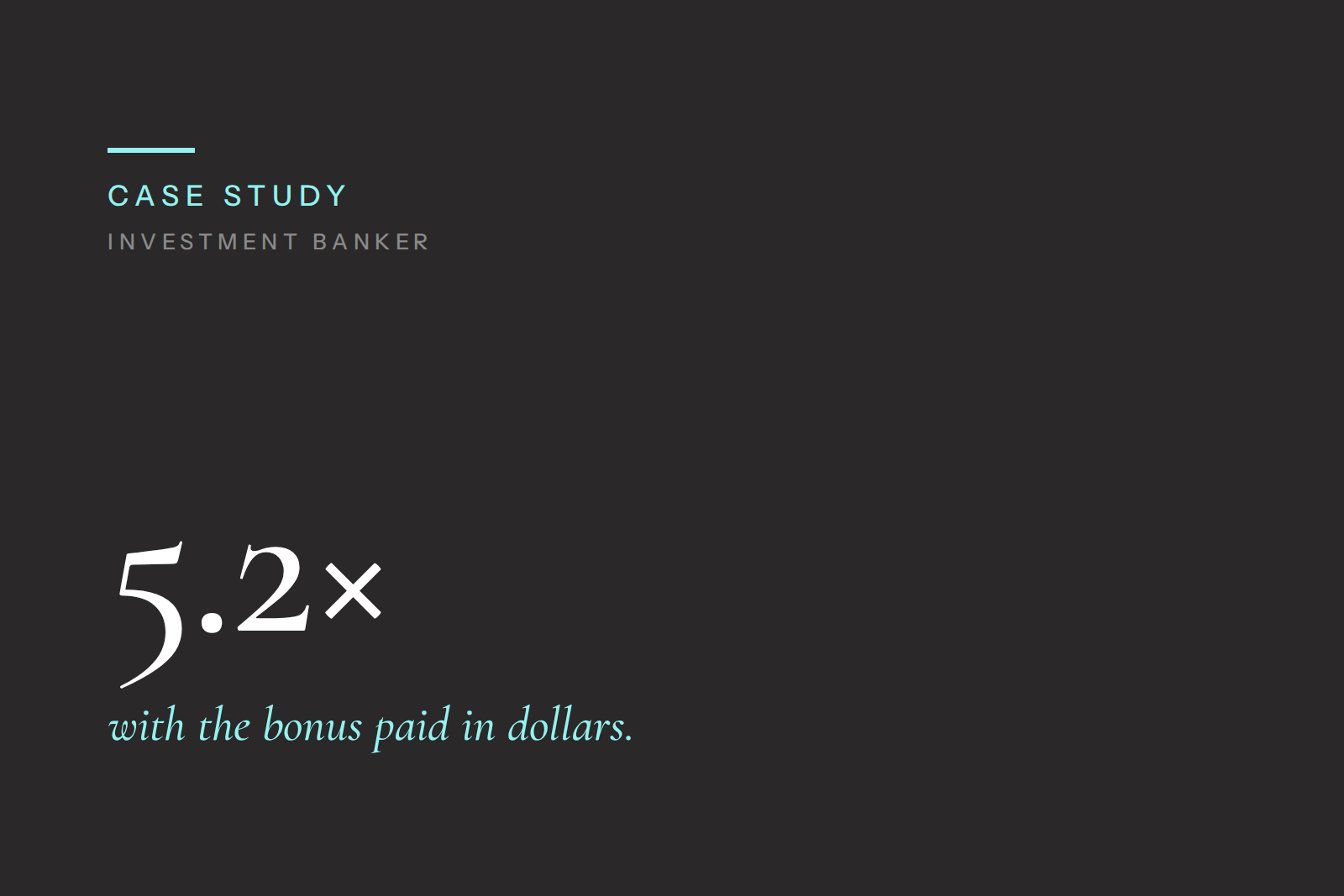

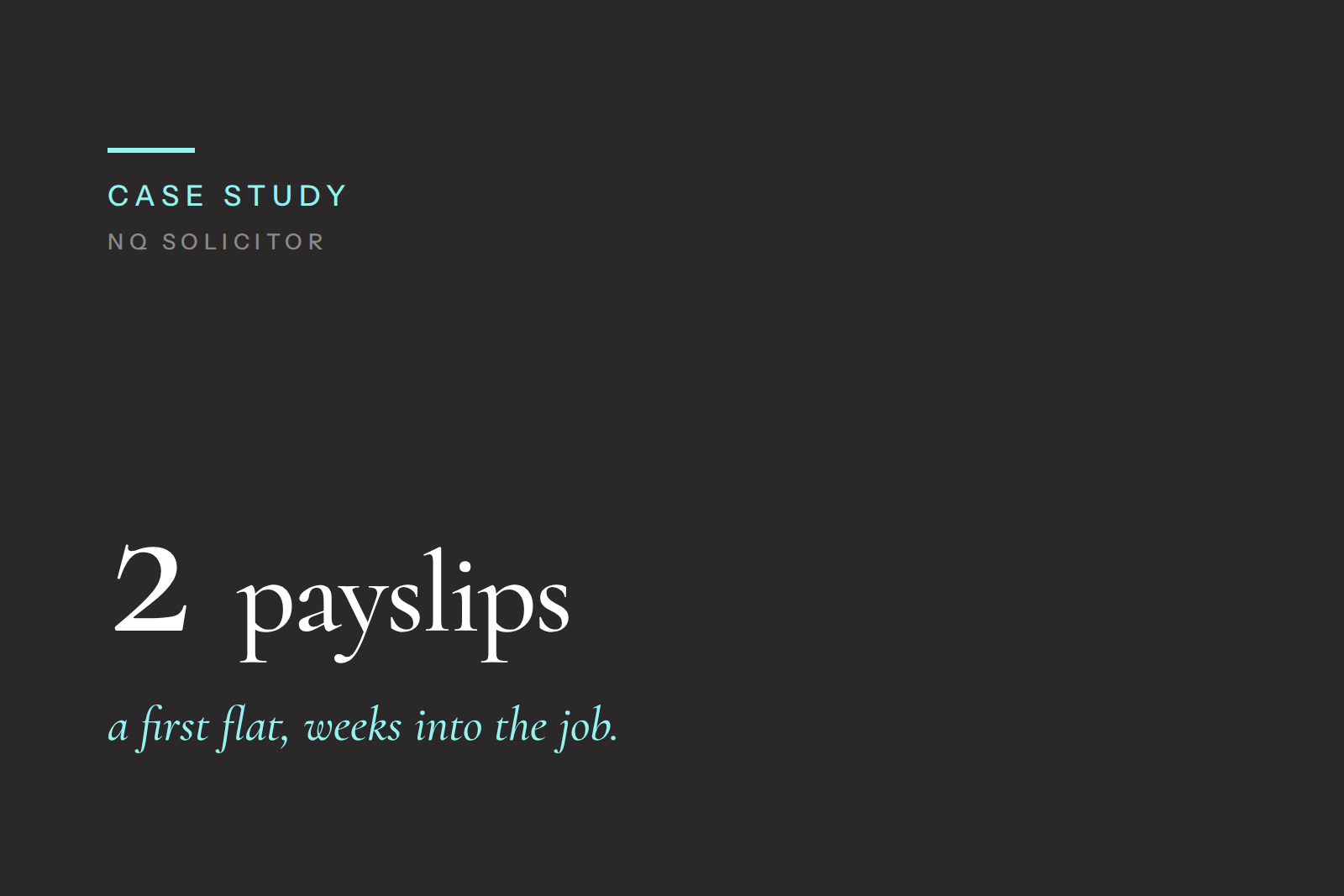

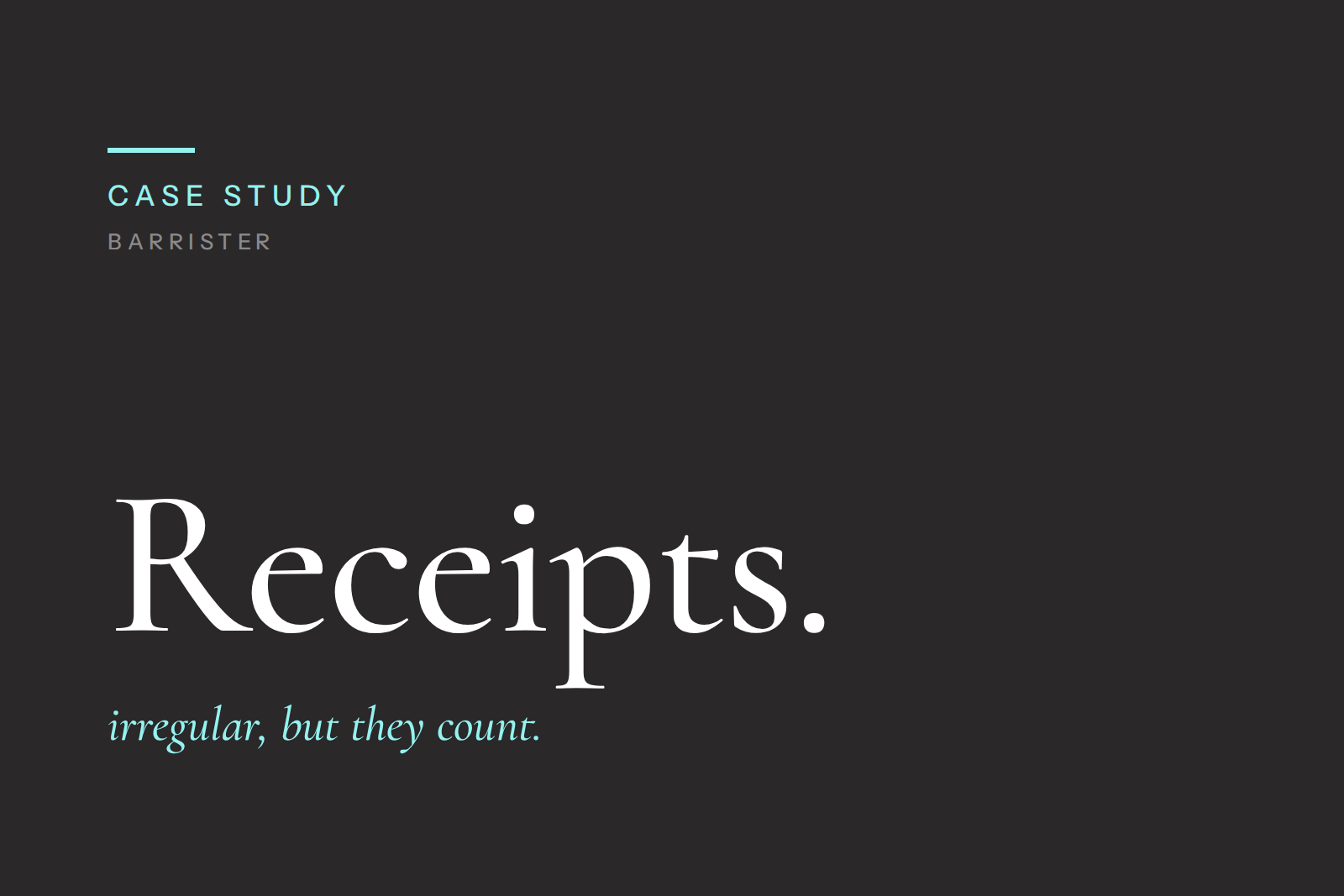

C A S E S T U D I E SRecent client outcomes

I N S I G H T SLatest articles